Making sense of the world through data

The focus of this blog is #data #bigdata #dataanalytics #privacy #digitalmarketing #AI #artificialintelligence #ML #GIS #datavisualization and many other aspects, fields and applications of data

Lies, damned lies and statistics!

In china it's all the same!

No one has ever exited a bubble by outgrowing it.

It will be so in China too.

The Chinese understand this of course which is why so much money is looking for a safe haven outside the country.

Official figures tell us that China is growing at 6.4% per year. But trade numbers are negative and electricity production static! Conversely, what is growing at double digits is money supply.

If there is a recession in the coming months as seems likely, it is in the economic numbers of the countries most dependent on trade with China such as Korea, Singapore and Hong Kong that it will show itself first.

Authored by John Rubino On ZeroHedge 21Apr2019 https://www.zerohedge.com/news/2019-04-20/chinas-fake-numbers-and-risk-they-pose-rest-world

Not so long ago, London Telegraph’s Ambrose

Evans-Pritchard was one of the handful of must-read financial

journalists. He probably still is, but since he disappeared behind the

Telegraph’s pay wall his work is invisible to non-subscribers, only

emerging when a free outlet runs one of his stories.

That happened this morning when the Sydney Morning Herald carried his analysis of the financial Ponzi scheme that is China.

After taking on more debt in a single decade than any other

country ever — in the process helping to pull the US and Europe out of

the Great Recession — China recently shifted into an even higher gear,

creating a world record amount of credit in the most recent reporting month.

And – more important for headline writers and money managers – it reported exactly the right amount of GDP growth.

This brings to mind a long-ago interview in which economist Nouriel Roubini asserted that China just makes its numbers up, frequently reporting GDP immediately after the end of the period being measured, something that even the US can’t do.

But it’s one thing to for the rest of us to suspect and/or assert

that China is just giving the markets what they want to hear, and

another thing to understand the implications and explain them

coherently. Evans-Pritchard does this in his latest article.

China’s majestic and elegantly-stable GDP figures are best seen as an instrument of political combat.

Donald Trump says “trade wars are good and easy to win” if your foes

depend on your market and you can break them under pressure.

He proclaimed victory when the Shanghai equity index went into a swoon over the winter. This is Trumpian gamesmanship.

It is in China’s urgent interest to puncture such claims as trade

talks come to a head. Xi Jinping had to beat expectations with a

crowd-pleaser in the first quarter. The number was duly produced: 6.4 per cent. Let us all sing the March of the Volunteers. “Could it really be true?” asked Caixin magazine. This was a brave question in Uncle Xi’s evermore totalitarian regime.

Of course it is not true. Japan’s

manufacturing exports to China fell by 9.4 per cent in March (year on

year). Singapore’s shipments dropped by 8.7 per cent to China, 22 per

cent to Indonesia, and 27 per cent to Taiwan. Korea’s exports are down

8.2 per cent. The greater China sphere of east Asia is in the midst of an industrial recession.

Nomura’s forward-looking index still points to a deepening downturn.

“Those expecting a strong rebound in Asian export growth in coming

months could be in for disappointment,” said the bank.

China’s rebound is hard to square with its own internal data. Simon

Ward from Janus Henderson said nominal GDP growth – trickier to

manipulate – is still falling. It dropped to 7.4 per cent from 8.1 per

cent in the last quarter on 2018.

Household demand deposits fell by 1.1 per cent last month.

This means that the growth rate of “true” M1 money is still at slump

levels. It has ticked up a fraction but this is nothing like

previous episodes of Chinese stimulus. It points towards stagnation into

late 2019. “Hold the champagne,” he said. A paper last month by Wei

Chen and Chang-Tai Tsieh for the Brookings Institution – “A Forensic

Examination of China’s National Accounts” – concluded that GDP growth has been overstated by 1.7 per cent a year on average since 2006. They used satellite data to track night lights in manufacturing zones, railway cargo volume, and so forth.

“Local officials are rewarded for meeting growth and investment targets,” they said. “Therefore, it is not surprising that local governments also have an incentive to skew the statistics.”

Liaoning – a Spain-sized province in the north – recently corrected

its figures after an anti-corruption crackdown exposed grotesque abuses.

Estimated GDP was cut by 22 per cent. You get the picture.

Bear in mind that if China’s economy is a fifth or a quarter smaller

than claimed it implies that the total debt ratio is not 300 per cent of

GDP (IIF data) but closer to 400 per cent. If China’s growth rate is

1.7 per cent lower – and falling every year – the country is less able

to rely on nominal GDP expansion whittling away the liabilities.

Debt dynamics take an ugly turn – just at a time when the working-age

population is contracting by two million a year. The International

Monetary Fund says China needs (true) growth of 5 per cent to prevent a

rising ratio of bad loans in the banking system.

China bulls in the West do not dispute most of this. But they say

that what matters is the “direction” of the data, and this is looking

better. Stimulus is flowing through. It gained traction in March with an

8.5 per cent bounce in industrial output – though sceptics suspect that

VAT changes led to front-loading. Suddenly the words “green shoots” are

on everybody’s lips.

The thinking is that China will rescue Europe. Optimists are

doubling down on another burst of global growth, clinched by the

capitulation of the US Federal Reserve. It will be a repeat of the

post-2016 recovery cycle.

Personally, I don’t believe this happy narrative. But what I do

respect after observing late-cycle psychology over four decades – and

having turned bearish too early during the dotcom boom – is that

investors latch onto good news with alacrity during the final phase of a

long expansion. A filtering bias creeps in.

So sticking my neck out, let me hazard that heady optimism will lead

to a rally on asset markets until the economic damage below the

waterline becomes clear.

Let us concede that Beijing has opened its fiscal floodgates to some

degree over recent weeks. Broad credit grew by $US430 billion ($601

billion) in March alone. Business tax cuts were another $US300 billion.

Bond issuance by local governments was pulled forward for extra impact.

But once you strip out the offsets, it is far from clear that the

picture for 2019 has changed. Nor is it clear what can be achieved with more credit.

The IMF said in its Fiscal Monitor that the country now needs 4.1 yuan

of extra credit to generate one yuan of GDP growth, compared to 3.5 in

2015, and 2.5 in 2009. The “credit intensity ratio” has worsened

dramatically. I stick to my view that the US will slump to stall speed

before China recovers. Europe is on the thinnest of ice. It has a broken

banking system. It is chronically incapable of generating its own

internal growth or taking meaningful measures in self-defence.

Momentum has fizzled out in all three blocs of the international system. We are entering the window of maximum vulnerability.

Lots of good data here – something notably lacking in most reporting on China’s “miracle.”

But the best — and scariest — single stat is the dramatic decline in

the marginal productivity of debt. China, like the US, is getting

progressively less bang for each newly-borrowed buck. There’s a point at

which new borrowing doesn’t just product less wealth but actually

destroys it. The US and China are heading that way fast, while Europe

might be there already.

We live in the age of data and consequently take it for granted that data speaks for itself.

But is this true?

We all have the experience of a discussion where however powerful our arguments are, whatever supportive data and examples we bring to the table, we get nowhere.

The Internet and its comfortable filter bubbles is said to be radicalizing our positions. But what if we are hardwired to not listen as the article below explains? And instead of listening with an open mind we critically scan other people's statements to strengthen our beliefs?

If that is the case as seems likely, we can either despair to ever reason successfully with anyone or conversely learn psychological techniques to influence people and achieve our goals as many self improvement books advice.

This is the choice we have as individuals. But as a society we can do better. We can build systems such as the scientific method which insure that the truth can emerge through reproducibility or remember that long before our universities became credential distributing machines, they were institutions dedicated to learning and thinking, knowledge and rhetoric.

The dusty but fundamental process of "Thesis, anti-thesis and synthesis" is too long to fit in a twit but should remain the core of any serious discussion. Likewise understanding that bias is human and therefore affects everyone of us including ourselves is a good place to start and question our own certainties and convictions!

In 1975, researchers at Stanford invited a group of undergraduates to take part in a study about suicide. They were presented with pairs of suicide notes. In each pair, one note had been composed by a random individual, the other by a person who had subsequently taken his own life. The students were then asked to distinguish between the genuine notes and the fake ones.

Some students discovered that they had a genius for the task. Out of twenty-five pairs of notes, they correctly identified the real one twenty-four times. Others discovered that they were hopeless. They identified the real note in only ten instances.

As is often the case with psychological studies, the whole setup was a put-on. Though half the notes were indeed genuine—they’d been obtained from the Los Angeles County coroner’s office—the scores were fictitious. The students who’d been told they were almost always right were, on average, no more discerning than those who had been told they were mostly wrong.

In the second phase of the study, the deception was revealed. The students were told that the real point of the experiment was to gauge their responses to thinking they were right or wrong. (This, it turned out, was also a deception.) Finally, the students were asked to estimate how many suicide notes they had actually categorized correctly, and how many they thought an average student would get right. At this point, something curious happened. The students in the high-score group said that they thought they had, in fact, done quite well—significantly better than the average student—even though, as they’d just been told, they had zero grounds for believing this. Conversely, those who’d been assigned to the low-score group said that they thought they had done significantly worse than the average student—a conclusion that was equally unfounded.

“Once formed,” the researchers observed dryly, “impressions are remarkably perseverant.”

A few years later, a new set of Stanford students was recruited for a related study. The students were handed packets of information about a pair of firefighters, Frank K. and George H. Frank’s bio noted that, among other things, he had a baby daughter and he liked to scuba dive. George had a small son and played golf. The packets also included the men’s responses on what the researchers called the Risky-Conservative Choice Test. According to one version of the packet, Frank was a successful firefighter who, on the test, almost always went with the safest option. In the other version, Frank also chose the safest option, but he was a lousy firefighter who’d been put “on report” by his supervisors several times. Once again, midway through the study, the students were informed that they’d been misled, and that the information they’d received was entirely fictitious. The students were then asked to describe their own beliefs. What sort of attitude toward risk did they think a successful firefighter would have? The students who’d received the first packet thought that he would avoid it. The students in the second group thought he’d embrace it.

Even after the evidence “for their beliefs has been totally refuted, people fail to make appropriate revisions in those beliefs,” the researchers noted. In this case, the failure was “particularly impressive,” since two data points would never have been enough information to generalize from.

The Stanford studies became famous. Coming from a group of academics in the nineteen-seventies, the contention that people can’t think straight was shocking. It isn’t any longer. Thousands of subsequent experiments have confirmed (and elaborated on) this finding. As everyone who’s followed the research—or even occasionally picked up a copy of Psychology Today—knows, any graduate student with a clipboard can demonstrate that reasonable-seeming people are often totally irrational. Rarely has this insight seemed more relevant than it does right now. Still, an essential puzzle remains: How did we come to be this way?

In a new book, “The Enigma of Reason” (Harvard), the cognitive scientists Hugo Mercier and Dan Sperber take a stab at answering this question. Mercier, who works at a French research institute in Lyon, and Sperber, now based at the Central European University, in Budapest, point out that reason is an evolved trait, like bipedalism or three-color vision. It emerged on the savannas of Africa, and has to be understood in that context.

Stripped of a lot of what might be called cognitive-science-ese, Mercier and Sperber’s argument runs, more or less, as follows: Humans’ biggest advantage over other species is our ability to coöperate. Coöperation is difficult to establish and almost as difficult to sustain. For any individual, freeloading is always the best course of action. Reason developed not to enable us to solve abstract, logical problems or even to help us draw conclusions from unfamiliar data; rather, it developed to resolve the problems posed by living in collaborative groups.

“Reason is an adaptation to the hypersocial niche humans have evolved for themselves,” Mercier and Sperber write. Habits of mind that seem weird or goofy or just plain dumb from an “intellectualist” point of view prove shrewd when seen from a social “interactionist” perspective.

Consider what’s become known as “confirmation bias,” the tendency people have to embrace information that supports their beliefs and reject information that contradicts them. Of the many forms of faulty thinking that have been identified, confirmation bias is among the best catalogued; it’s the subject of entire textbooks’ worth of experiments. One of the most famous of these was conducted, again, at Stanford. For this experiment, researchers rounded up a group of students who had opposing opinions about capital punishment. Half the students were in favor of it and thought that it deterred crime; the other half were against it and thought that it had no effect on crime.

The students were asked to respond to two studies. One provided data in support of the deterrence argument, and the other provided data that called it into question. Both studies—you guessed it—were made up, and had been designed to present what were, objectively speaking, equally compelling statistics. The students who had originally supported capital punishment rated the pro-deterrence data highly credible and the anti-deterrence data unconvincing; the students who’d originally opposed capital punishment did the reverse. At the end of the experiment, the students were asked once again about their views. Those who’d started out pro-capital punishment were now even more in favor of it; those who’d opposed it were even more hostile.

If reason is designed to generate sound judgments, then it’s hard to conceive of a more serious design flaw than confirmation bias. Imagine, Mercier and Sperber suggest, a mouse that thinks the way we do. Such a mouse, “bent on confirming its belief that there are no cats around,” would soon be dinner. To the extent that confirmation bias leads people to dismiss evidence of new or underappreciated threats—the human equivalent of the cat around the corner—it’s a trait that should have been selected against. The fact that both we and it survive, Mercier and Sperber argue, proves that it must have some adaptive function, and that function, they maintain, is related to our “hypersociability.”

Mercier and Sperber prefer the term “myside bias.” Humans, they point out, aren’t randomly credulous. Presented with someone else’s argument, we’re quite adept at spotting the weaknesses. Almost invariably, the positions we’re blind about are our own.

A recent experiment performed by Mercier and some European colleagues neatly demonstrates this asymmetry. Participants were asked to answer a series of simple reasoning problems. They were then asked to explain their responses, and were given a chance to modify them if they identified mistakes. The majority were satisfied with their original choices; fewer than fifteen per cent changed their minds in step two.

In step three, participants were shown one of the same problems, along with their answer and the answer of another participant, who’d come to a different conclusion. Once again, they were given the chance to change their responses. But a trick had been played: the answers presented to them as someone else’s were actually their own, and vice versa. About half the participants realized what was going on. Among the other half, suddenly people became a lot more critical. Nearly sixty per cent now rejected the responses that they’d earlier been satisfied with.

This lopsidedness, according to Mercier and Sperber, reflects the task that reason evolved to perform, which is to prevent us from getting screwed by the other members of our group. Living in small bands of hunter-gatherers, our ancestors were primarily concerned with their social standing, and with making sure that they weren’t the ones risking their lives on the hunt while others loafed around in the cave. There was little advantage in reasoning clearly, while much was to be gained from winning arguments.

Among the many, many issues our forebears didn’t worry about were the deterrent effects of capital punishment and the ideal attributes of a firefighter. Nor did they have to contend with fabricated studies, or fake news, or Twitter. It’s no wonder, then, that today reason often seems to fail us. As Mercier and Sperber write, “This is one of many cases in which the environment changed too quickly for natural selection to catch up.”

Steven Sloman, a professor at Brown, and Philip Fernbach, a professor at the University of Colorado, are also cognitive scientists. They, too, believe sociability is the key to how the human mind functions or, perhaps more pertinently, malfunctions. They begin their book, “The Knowledge Illusion: Why We Never Think Alone” (Riverhead), with a look at toilets.

Virtually everyone in the United States, and indeed throughout the developed world, is familiar with toilets. A typical flush toilet has a ceramic bowl filled with water. When the handle is depressed, or the button pushed, the water—and everything that’s been deposited in it—gets sucked into a pipe and from there into the sewage system. But how does this actually happen?

In a study conducted at Yale, graduate students were asked to rate their understanding of everyday devices, including toilets, zippers, and cylinder locks. They were then asked to write detailed, step-by-step explanations of how the devices work, and to rate their understanding again. Apparently, the effort revealed to the students their own ignorance, because their self-assessments dropped. (Toilets, it turns out, are more complicated than they appear.)

Sloman and Fernbach see this effect, which they call the “illusion of explanatory depth,” just about everywhere. People believe that they know way more than they actually do. What allows us to persist in this belief is other people. In the case of my toilet, someone else designed it so that I can operate it easily. This is something humans are very good at. We’ve been relying on one another’s expertise ever since we figured out how to hunt together, which was probably a key development in our evolutionary history. So well do we collaborate, Sloman and Fernbach argue, that we can hardly tell where our own understanding ends and others’ begins.

“One implication of the naturalness with which we divide cognitive labor,” they write, is that there’s “no sharp boundary between one person’s ideas and knowledge” and “those of other members” of the group.

This borderlessness, or, if you prefer, confusion, is also crucial to what we consider progress. As people invented new tools for new ways of living, they simultaneously created new realms of ignorance; if everyone had insisted on, say, mastering the principles of metalworking before picking up a knife, the Bronze Age wouldn’t have amounted to much. When it comes to new technologies, incomplete understanding is empowering.

Where it gets us into trouble, according to Sloman and Fernbach, is in the political domain. It’s one thing for me to flush a toilet without knowing how it operates, and another for me to favor (or oppose) an immigration ban without knowing what I’m talking about. Sloman and Fernbach cite a survey conducted in 2014, not long after Russia annexed the Ukrainian territory of Crimea. Respondents were asked how they thought the U.S. should react, and also whether they could identify Ukraine on a map. The farther off base they were about the geography, the more likely they were to favor military intervention. (Respondents were so unsure of Ukraine’s location that the median guess was wrong by eighteen hundred miles, roughly the distance from Kiev to Madrid.)

Surveys on many other issues have yielded similarly dismaying results. “As a rule, strong feelings about issues do not emerge from deep understanding,” Sloman and Fernbach write. And here our dependence on other minds reinforces the problem. If your position on, say, the Affordable Care Act is baseless and I rely on it, then my opinion is also baseless. When I talk to Tom and he decides he agrees with me, his opinion is also baseless, but now that the three of us concur we feel that much more smug about our views. If we all now dismiss as unconvincing any information that contradicts our opinion, you get, well, the Trump Administration.

“This is how a community of knowledge can become dangerous,” Sloman and Fernbach observe. The two have performed their own version of the toilet experiment, substituting public policy for household gadgets. In a study conducted in 2012, they asked people for their stance on questions like: Should there be a single-payer health-care system? Or merit-based pay for teachers? Participants were asked to rate their positions depending on how strongly they agreed or disagreed with the proposals. Next, they were instructed to explain, in as much detail as they could, the impacts of implementing each one. Most people at this point ran into trouble. Asked once again to rate their views, they ratcheted down the intensity, so that they either agreed or disagreed less vehemently.

Sloman and Fernbach see in this result a little candle for a dark world. If we—or our friends or the pundits on CNN—spent less time pontificating and more trying to work through the implications of policy proposals, we’d realize how clueless we are and moderate our views. This, they write, “may be the only form of thinking that will shatter the illusion of explanatory depth and change people’s attitudes.”

One way to look at science is as a system that corrects for people’s natural inclinations. In a well-run laboratory, there’s no room for myside bias; the results have to be reproducible in other laboratories, by researchers who have no motive to confirm them. And this, it could be argued, is why the system has proved so successful. At any given moment, a field may be dominated by squabbles, but, in the end, the methodology prevails. Science moves forward, even as we remain stuck in place.

In “Denying to the Grave: Why We Ignore the Facts That Will Save Us” (Oxford), Jack Gorman, a psychiatrist, and his daughter, Sara Gorman, a public-health specialist, probe the gap between what science tells us and what we tell ourselves. Their concern is with those persistent beliefs which are not just demonstrably false but also potentially deadly, like the conviction that vaccines are hazardous. Of course, what’s hazardous is not being vaccinated; that’s why vaccines were created in the first place. “Immunization is one of the triumphs of modern medicine,” the Gormans note. But no matter how many scientific studies conclude that vaccines are safe, and that there’s no link between immunizations and autism, anti-vaxxers remain unmoved. (They can now count on their side—sort of—Donald Trump, who has said that, although he and his wife had their son, Barron, vaccinated, they refused to do so on the timetable recommended by pediatricians.)

The Gormans, too, argue that ways of thinking that now seem self-destructive must at some point have been adaptive. And they, too, dedicate many pages to confirmation bias, which, they claim, has a physiological component. They cite research suggesting that people experience genuine pleasure—a rush of dopamine—when processing information that supports their beliefs. “It feels good to ‘stick to our guns’ even if we are wrong,” they observe.

The Gormans don’t just want to catalogue the ways we go wrong; they want to correct for them. There must be some way, they maintain, to convince people that vaccines are good for kids, and handguns are dangerous. (Another widespread but statistically insupportable belief they’d like to discredit is that owning a gun makes you safer.) But here they encounter the very problems they have enumerated. Providing people with accurate information doesn’t seem to help; they simply discount it. Appealing to their emotions may work better, but doing so is obviously antithetical to the goal of promoting sound science. “The challenge that remains,” they write toward the end of their book, “is to figure out how to address the tendencies that lead to false scientific belief.”

“The Enigma of Reason,” “The Knowledge Illusion,” and “Denying to the Grave” were all written before the November election. And yet they anticipate Kellyanne Conway and the rise of “alternative facts.” These days, it can feel as if the entire country has been given over to a vast psychological experiment being run either by no one or by Steve Bannon. Rational agents would be able to think their way to a solution. But, on this matter, the literature is not reassuring.

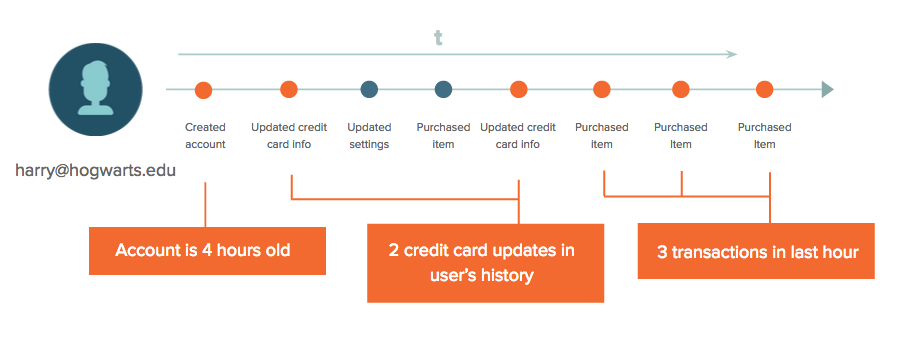

As discussed earlier, Chinese style credit scoring is coming to our shores, like it or not. Commercial and social aspects will be included. It is unavoidable. This subject should be more openly discussed!

We're All Being Judged By A Secret 'Trustworthiness' Score

Nearly

everything we buy, how we buy, and where we're buying from is secretly

fed into AI-powered verification services that help companies guard

against credit-card and other forms of fraud, according to the Wall Street Journal.

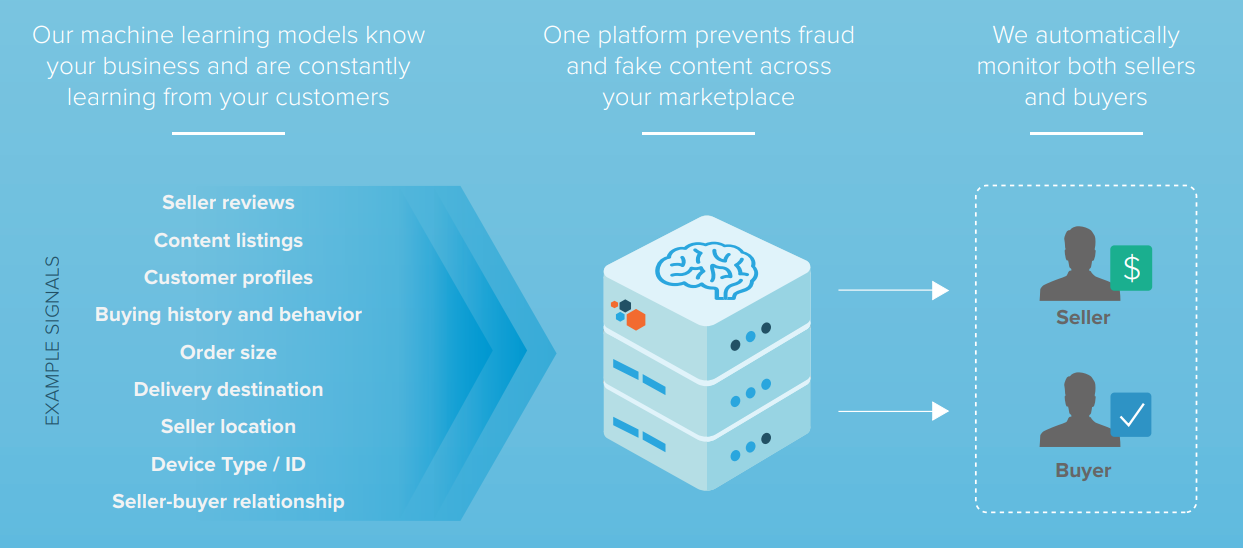

More than 16,000 signals are analyzed by a service called Sift,

which generates a "Sift score" ranging from 1 - 100. The score is used

to flag devices, credit cards and accounts that a vendor may want to

block based on a person or entity's overall "trustworthiness" score,

according to a company spokeswoman.

From the Sift website:

"Each time we get an event -- be it a page view or an API event -- we

extract features related to those events and compute the Sift Score.

These features are then weighed based on fraud we've seen both on your

site and within our global network, and determine a user's Score. There

are features that can negatively impact a Score as well as ones which

have a positive impact."

The system is similar to a credit score - except there's no way to find out your own Sift score.

Factors which contribute to one's Sift score (per the WSJ):

• Is the account new?

• Are there are a lot of digits at the end of an email address?

• Is the transaction coming from an IP address that’s unusual for your account?

• Is the transaction coming from a region where there are a lot of hackers, such as China, Russia or Eastern Europe?

• Is the transaction coming from an anonymization network?

• Is the transaction happening at an odd time of day?

• Has the credit card being used had chargebacks associated with it?

• Is the browser different from what you typically use?

• Is the device different from what you typically use?

• Is the cadence of the way you typed out your password typical for you? (tracked by some advanced systems) Sources: Sift, SecureAuth, Patreon

The system is used by companies such as Airbnb, OpenTable, Instacart and LinkedIn.

Companies that use services like this often mention it in their privacy policies—see Airbnb’s here—but how many of us realize our account behaviors are being shared with companies we’ve never heard of, in the name of security? How

much of the information one company shares with these fraud-detection

services is used by other clients of that service? And why can’t we

access any of this data ourselves, to update, correct or delete it?

According to Sift and competitors such as SecureAuth, which has a similar scoring system, this practice complies with regulations such as the European Union’s General Data Protection Regulation, which mandates that companies don’t store data that can be used to identify real human beings unless they give permission.

Unfortunately GDPR, which went into effect a year ago, has rules that

are often vaguely worded, says Lisa Hawke, vice president of security

and compliance at the legal tech startup Everlaw. All of this will have to get sorted out in court, she adds. -Wall Street Journal

In order to optimize scoring "Sift regularly evaluates the

performance of our models and tries to minimize bias and variance in

order to maximize accuracy," according to a spokeswoman.

"While we don’t perform audits of our customers’ systems for bias, we

enable the organizations that use our platform to have as much

visibility as possible into the decision trees, models or data that were

used to reach a decision," according to SecureAuth Vice President and

chief security architect Stephen Cox. "In some cases, we may not be fully aware of the means by which our services and products are being used within a customer’s environment." Not always right

While Sift and SecureAuth strive for accuracy, sometimes it's difficult to decipher authentic purchasing behavior from fraud.

"Sometimes your best customers and your worst customers look the

same," said Jacqueline Hart, head of trust and safety at Patreon - a

site used by artists and creators to allow benefactors to support them.

"You can have someone come in and say I want to pledge $10,000 and

they’re either a fraudster or an amazing patron of the arts," Hart

added.

If an account is rejected due to its Sift score, Patreon directs the

benefactor to the company's trust and safety team. "It’s an important

way for us to find out if there are any false positives from the Sift

score and reinstate the account if it shouldn’t have been flagged as

high risk," said Hart.

There are many potential tells that a transaction is fishy. “The amazing thing to me is when someone fails to log in effectively, you know it’s a real person,”

says Ms. Hart. The bots log in perfectly every time. Email addresses

with a lot of numbers at the end and brand new accounts are also more

likely to be fraudulent, as are logins coming from anonymity networks

such as Tor. These services also learn from every transaction across their entire system, and compare data from multiple clients. For instance, if

an account or mobile device has been associated with fraud at, say,

Instacart, that could mark it as risky for another company, say Wayfair—even if the credit card being used seems legitimate, says a Sift spokeswoman. -Wall Street Journal

A person's Sift score is constantly changing based on that user's

behavior, and any new information the system gathers about them,

according to the spokeswoman. From Sift:

We learn in real-time, which means Scores are constantly being

recalculated based on new knowledge of fraudulent users and

patterns. For example, when someone logs in, we've found out a lot of

information in the meantime about suspicious devices, IP addresses,

shipping addresses, etc., based on the activity of other users. Add this

to the fact that there may have been some new labeled users since their

last login, and the scores can sometimes have a significant change.

This is also more likely if the user hasn't had much activity on your

site. -Sift.com

While Sift judges whether or not one can be trusted, there's no file

with your name on it that it can produce for review - because it doesn't need your name to analyze your behavior, according to the report - which seems like total BS.

"Our customers will send us events like ‘account created,’ ‘profile

photo uploaded,’ ‘someone sent a message,’ ‘review written,’ ‘an item

was added to shopping cart," says Sift CEO Jason Tan.

It’s technically possible to make user data difficult or impossible to link to a real person. Apple and others say they take steps to prevent such “de-anonymizing.”Sift

doesn’t use those techniques. And an individual’s name can be among the

characteristics its customers share with it in order to determine the

riskiness of a transaction.

In the gap between who is taking responsibility for user data—Sift or

its clients—there appears to be ample room for the kind of slip-ups

that could run afoul of privacy laws. Without an audit of such a system

it’s impossible to know. Companies live under increasing threat of

prosecution, but as just-released research on biases in Facebook ’s advertising algorithm suggest, even the most sophisticated operators don’t seem to be fully aware of how their systems are behaving. -Wall Street Journal

"I would argue that in our desire to protect privacy, we have to be careful, because are we going to make it impossible for the good guys to perform the necessary function of security?" asks Anshu Sharma - co-founder of Clearedin, a startup which helps companies avoid falling victim to email phishing attacks.

His solution? Transparency. When a company rejects a potential

customer based on their Sift score, for example, it should explain why -

even if that exposes how the scoring system works.

China has already won! But we are fighting the wrong fight!

By Shelly Palmer on the Shelly Palmer Blog

7 April 2019

https://www.shellypalmer.com/2019/04/china-already-won-fighting-wrong-fight/

This is an interesting and important article to which I agree almost completely.

No of course, China has not won yet but they are on their way as Shelly Palmer explains and it is mostly thanks to their social and political system which welcomes this new technology.

Is it a good thing?

"This is NOT the subject of the article!"

But it is an essential question that we must address.

Do we want to live in a hyper polluted dystopia of credit score and pre-crime police state?

The more I discuss with AI experts the clearer it becomes that AI will be us! It is us, minus the ability to lie, (Should we make this the new Turing test?) and a few other human characteristics we do not understand well, plus some new emerging factors we may never control fully.

This is the discussion we need to have while we implement these new technologies! This is far more important than trade policies which modifications would bring more ills than goods to the aspects of our lives people are concerned with (work, environment, neighborhoods)

The next industrial revolution (more like an intellectual revolution this time), will probably be "made in China". Can we work with the Chinese and tame the dragon or do we get an efficient and unstoppable creature from hell?

This is the question we must answer. Limitations on trade, data flows and AI without understanding the consequences is an answer but I agree with Shelly Palmer that it may not be a winning solution.

China has already won! But we are fighting the wrong fight!

While I was in China this past week, Google dissolved its 10-day-old

AI ethics council. Why? Because of AI bias, a super-important,

completely misnamed topic. There’s no such thing as AI bias. It’s human

bias that is being inflicted on AI as we try to teach our flexible moral

codes to inanimate computational engines that have no context. “Hey,

you look great today!” we happily say to someone who looks terrible.

“Wow! Your home is just beautiful,” we say with as much sincerity as

humanly possible while observing the tasteless interior decorations of a

friend’s home. Your spouse (trying to make you a better human being):

“Did you call your mother this week?” You (lying through your teeth): “I

tried, but it went straight to voicemail and I didn’t leave a message.”

White lies? True lies? Just plain lies? Humans lie because there are

evolutionarily stable reasons to do so.

Richard Dawkins posits that we learn to lie as infants as we figure

out what kind of crying will get our mother’s immediate attention.

According to Sun Tsu, “War is the art of deception.” To be human is to

lie. On the other hand, to be a machine (forgive the anthropomorphism)

is to calculate probabilities to determine the best (mathematically

truest) answer. Machines don’t lie by themselves; they must be

specifically taught to do so (by humans). For example: Libratus,

Carnegie Mellon University’s championship-level Texas Hold’em–playing AI

system, bluffs like a pro. BTW, bluffs are lies.

Do we need an AI bias council? Sure. It’s a great idea. Will it help

the United States maintain its position as the technological leader of

planet Earth? No. China has already won the AI race, and the United

States may not have a way to catch up.

We can chat all we like about human biases creating AI biases with

our Western cultural ideology, but if there is going to be anything like

an AI bias council, it should probably be held in Beijing, Shanghai, or

Shenzhen. Chinese cultural and political norms are going to have a much

bigger influence over AI bias than anything we do here in America.

I spend quite a bit of time working with multinational corporations

that operate in APAC (Asia-Pacific). This past week, I got to spend some

quality time with Chinese colleagues working on the most cutting-edge

AI systems I have ever seen in action. The data sets are astronomical,

the access to data is unfettered, the population is practically 100

percent mobile-only, and the competition is so fierce, only the very

best systems have a chance.

Imagine if you had every data point about everyone and you had the

ability to turn that data into action. You walk to a street corner and

your phone knows exactly where you are, what you are looking for, and

where to direct you. No ads, just information you need when you need it.

Then, you do the transaction and pay with your phone, get your

ride-share with your phone, give a homeless person a donation with your

phone. Keep imagining, and you still won’t get to where China is today,

let alone where it’s headed. Oh, BTW, the government sees 100 percent of

the data that you get to analyze. (But that’s for another article.)

Europe enacted GDPR to prevent what’s happening in China. The US

government has called FAANG and other tech companies to testify before

Congress so that America can figure out how to enact its own version of

GDPR. While Europe and America compare notes about what data privacy may

or may not mean, in Shanghai, what I have described above is about 5

percent of what people can do with the BAT (Baidu, Alibaba, and Tencent)

apps installed on their smartphones. We’re talking about it; China is

doing it.

Yes, there are still two Chinas: the new China with bright shining

(though smoggy) cities and amazing tech, and the countryside where some

communities don’t have electricity or running water. But on balance, the

tech in China (and its path to the future as a result of China’s data

policies) will make it just about impossible for America to catch up,

let alone compete.

(Please do not write to me about social scoring and human right

violations in China. That is not what this article is about, and I am

not commenting on or condoning China’s human rights policies. This

article is about AI bias, human bias, and how far China is ahead in the

AI race – the “space race” of this century.)

Is there anything we can do?

I believe there is something we can do. First, we need to stop

thinking about the “AI race” and simply agree that technological

progress will continue at an exponential rate. Next, we need to reframe

the China vs. America conflict to what it really is: human beings (all

human beings) planning for a future where tools not only “think,” they

make decisions that will impact how we (all of us humans) spend our

days.

We can learn to work together. My friends and colleagues in China are

productivity machines! They work incessantly. Not only do they work

hard, they work smart. It is humbling.

My friends in China are super-competitive, because they have to be.

But they are also open to new ideas, especially cultural ones. To a

person, they love to learn, and as I have come to understand over the

past 30 years working with some wonderful people across APAC, they are

simply trying to live respectable, happy lives.

AI, writ large, is already changing everything. The technology is

going to affect everyone. So, before we get into an economically

devastating game of dueling AIs, let’s put our own biases aside and get

some multinational, cross-cultural, cross-industry councils together to

chat about how humans should treat humans, how humans should treat

machines, and topically, how machines should treat humans.

This article comes from the Washington's Blog, an interesting blog in its own right but is originally written by Charles Hugh Smith, one of the most original source of interesting ideas I have found on the net.

https://www.oftwominds.com/blog.html

It is followed by my own comments.

The Hidden Cost of Losing Local Mom and Pop Businesses

There is much more to this article than

first meets the eye:

In a Tokyo neighborhood’s last sushi

restaurant, a sense of loss

“Eiraku is the last surviving sushi bar in

this cluttered neighborhood of steep cobblestoned hills and cherry trees unseen

on most tourist maps of Tokyo. Caught between the rarified world of $300

omakase dinners and the brutal efficiency of chain-restaurant fish, mom-and-pop

shops like it are fast disappearing.

Chef Masatoshi Fukutsuna and his wife,

Mitsue, smile without a word. In the 35 years since they opened up shop, the

couple has seen many of their friends move away for a job or family, only to

return decades later, often without the job or the family, their absence

unspoken.

Absence is a part of life here on what

remains of the Medaka shopping street, a road so narrow that cars have to drive

up onto the sidewalk to let another vehicle pass.

Once the sky turns pink and the sun sets,

the street descends into shadow, save for the faintest glow from halogen lamp

posts.

It’s a neighborhood in twilight. More like

it are scattered across this city, their corner cafes and stores far from the

neon blare of the famous shopping districts. The number of independent,

family-owned sushi bars in Tokyo has halved to 750 in the last decade, a trade

association says, driven out of business by fast-food joints and a younger

generation that doesn’t want to inherit them.

“People would rather pay 100 yen for a

plate of sushi at a really cheap place or they’d shell out tens of thousands of

yen to go to a famous sushi restaurant in Ginza that they heard about on

television,” says the chef, absentmindedly changing the channel of the TV. “But

places like ours, shops that are right in the middle, we just can’t seem to

survive.”

In the U.S., and presumably elsewhere,

there are other financial pressures on small businesses: the complexity of

compliance with the ever-increasing thicket of regulations is constantly

increasing, as are taxes and fees as local government seeks to extract more

revenue from the small-business tax donkeys.

These increases in costs while revenues sag

as customers seek cheaper chain meals or simply stop going out at all are a

double-whammy.

But look at what’s lost in the demise of

local small businesses:

— The loss of neighborhood character and

variety, replaced by homogenized chains and lifeless shuttered storefronts.

— the loss of food that’s been prepared by

hand with real ingredients.

— the loss of neighborhood cohesion and

social circles; residents who were once recognized as individuals and who

belonged to loose but important social circles are unknown in faceless chain

outlets.

— the loss of local employment. Employees

in chain outlets commute from distant places, and their hours and locations may

change, making it impossible to know local residents.

— the loss of walkable, interesting

neighborhoods. What’s there to explore or provide interest in a string of steel

and glass chain outlets?

— the loss of local social gathering

places. Once local neighborhood places are lost, people gravitate to McDonalds

or similar chain outlets because McDonalds will not hurry customers away from

its tables. In some cultures, the American fast-food outlets are attractive

because they are clean, well-lit and class-neutral: they serve every customer

with well-trained politeness: the service is as uniform as the food.

The 2013 book Food and Culture: A Reader

has an interesting essay by Yungxiang Yan about the social and class structure

of McDonalds in China: Of Hamburger and Social Space: Consuming McDonald’s in

Beijing.

The essay helps us understand why Western

fast-food outlets have achieved such extraordinary popularity around the world:

they provide inviting social spaces, not just uniform, consistent,

reasonable-cost food.

Needless to say, American fast-food outlets

are engineered to provide these social-space and class/gender-neutral assets as

well as carefully engineered menu selections; in many cultures, McDonald’s

offers women and a safe and acceptable place to gather and socialize. fast-food

outlets are popular with students for similar reasons.

My point here is not to say that fast-food

outlets don’t serve a positive social role; the point is what fast-food outlets

provide is not a 100% replacement for what’s lost as local Mom and Pop stores

and cafes vanish.

What cannot be replaced by corporate chains

is neighborhood character and variety: once locally owned and operated

businesses wither and die, the neighborhood looks like other every other

redeveloped, homogenized street around the world.

This is fine for those who want an

anonymous, impersonal meal and table, but an anonymous, impersonal meal and

table is now available from Beijing to Belfast in a monotonous uniformity of

menus and spaces.

What’s scarce and thus valuable are not

fast-food outlets; what’s scarce and valuable are walkable, diverse

neighborhoods of locally owned and operated stores and cafes which offer social

refreshment and bonds as well as home-cooked meals.

Comments:

Compared to many other cities around the world, (The worst homogenization is probably found in the UK high streets) Tokyo is relatively spared as just outside its main arteries, the city has retained many traditional neighborhoods. But it is nevertheless plagued by chain stores and franchise business as elsewhere. It is unfortunately unavoidable. The playing field is so skewed in favor of these brands that it is in fact a miracle that anything else still exists.

Franchise business often employ former shop owners who could not survive on their own and were obliged to join in. They can close and open at will, lose money for years (it is usually not their money) and go locally bankrupt. Often the main chains have several competing outlets within walking distance.

This said, their homogenized products and services are sometimes worse but often better than what came before. They strive to improve on a global scale which small stores could not. It is a complex equation with many elements. Not all being negative.

{kind=link}