I always find it difficult to explain to people why I am so pessimistic about the prospects of the world and why I expect leaders to play for broke as they know the depth of the mess they have created.

Japan is and has always been the canary in the coal mine. It is obvious for anyone who understand how finance truly works that 2008 will never happen again. Would a bank go under like Bear Stearn or Lehman, the authorities would immediately flood the market with liquidity to make sure that a "freeze" is avoided.

Problem solved then? You wish! By doing the above what you have done is simply made the problem systemic and transferred the risk. To whom exactly? That, we will know only when we see it. But at some stage, something, somewhere is going to break. And it's going to be so big and systemic that there will be nothing we can do about it. Suddenly the whole house of cards will be going down. Accounts will be frozen and everything will be repriced. This is not me saying this but most market insiders at this late stage. This will be the true price of the 16+ years of virtual prosperity the West has bought on credit.

Which is the REAL reason why war is unavoidable. Incomes will be halved, services suspended, pensions paid with beans, inflation through the roof. How could any "democratic" country sustain such a shock? This is of course impossible so it won't happen. By later 2025 at the latest most countries in the West will have exited their "democratic" phase. The easiest way for people to accept this is a state of emergency. It looks like bird flu or whatever manufactured virus is unleashed will not be enough. Well, war it shall be then! I do not see any other option and unfortunately neither seems to do our current leadership. (The ones behind the curtain who control the financial system, not the clowns on television!)

The Music Just Stopped: Japan Banking Giant Norinchukin To Liquidate $63 Billion In Treasuries & European Bonds To Plug Massive Unrealized Losses

Last October, when the wounds from the March 2023 bank failures - which surpassed the global financial crisis in total assets and which sparked the latest Fed intervention, setting the market's nadir over the past 16 months - were still fresh, we made a non-consensus prediction: we said that since the Fed has once again backstopped the US financial system, "the next bank failure will be in Japan."

This prediction only got warmer two months later when, inexplicably, Japan's Norinchukin bank, best known as Japan's CLO whale, was quietly added to the list of counterparties for the Fed's Standing Repo Facility, a/k/a the Fed's foreign bank bailout slush fund.

But if that was the first, and still distant, sign that something was very wrong at one of Japan's biggest banks (Norinchukin is Japan's 5th largest bank with $840 billion in assets) today the proverbial canary stepped on a neutron bomb inside the Japanese coalmine, because according to Nikkei, Norinchukin Bank "will sell more than 10 trillion yen ($63 billion) of its holdings of U.S. and European government bonds during the year ending March 2025 as it aims to stem its losses from bets on low-yield foreign bonds, a main cause of its deteriorating balance sheet, and lower the risks associated with holding foreign government bonds."

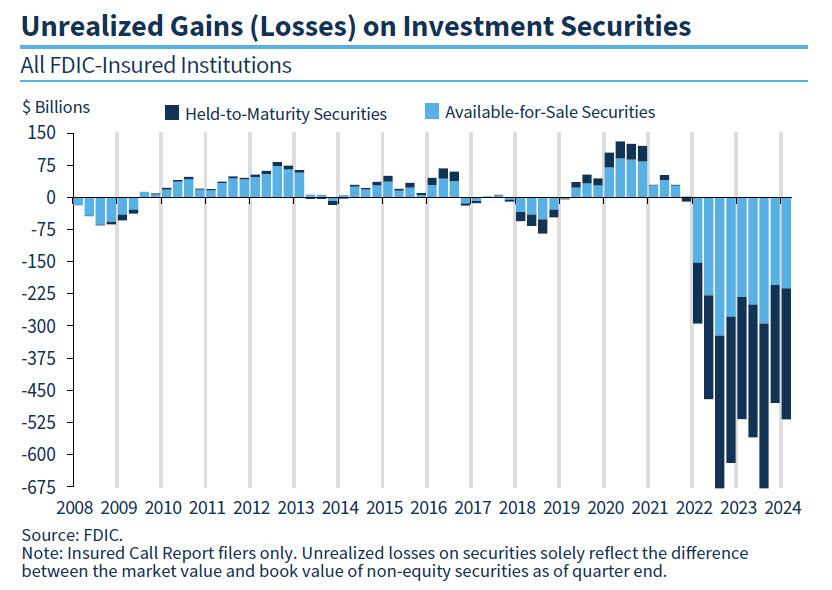

See, what's happened in Japan is not that different from what is happening in the US, where as the FDIC keeps reminding us quarter after quarter, US banks are still sitting on over half a trillion dollars in unrealized losses, as a result of the huge jump in interest rates which has blown up the banks' long-duration fixed income holdings, sending them trading far below par and forcing banks (and the Fed, see BTFP) to come up with creative ways of shoving these massive losses under the rug.

And while Japanese rates have barely budged - the BOJ only just raised rates for the first time in decades in April - the move is already cascading into the form of huge losses for domestic banks, which have been hammered twice as hard due to their holdings of offshore debt which until 2021 was viewed as risk free, only to blow up in everyone's face two years ago when the bull market since the early 1980s ended with a bang.

Enter Norinchukin: according to the Nikkei, the company's net loss for the year ending March 2025, which was previously forecast to top 500 billion yen, will rise to the 1.5 trillion yen level with the bond sales.

"We plan to sell low-yield [foreign] bonds in the amount of 10 trillion yen or more," Norinchukin Bank CEO Kazuto Oku told Nikkei, an amount just above $60 billion.

The bank, which previously was best known for being one of the world's most aggressive CLO investors - buys securities out of pension funds deposited by agriculture, forestry, and fisheries concerns.

Facing a problem that is very familiar to all US banks, Oku said the bank "acknowledged the need to drastically change its portfolio management" to reduce unrealized losses on its bonds, which totaled roughly 2.2 trillion yen as of the end of March. Oku explained bank's intention to shift its investments, saying, "We will reduce [sovereign] interest rate risk and diversify into assets that take on corporate and individual credit risk."

Now, if Nochu, as it is affectionately known by bankruptcy lawyers, was a US bank circa one year ago, it would not have to sell anything: it could just pledge all of its sharply depreciated bonds at the Fed's BTFP facility, and get a par value for them.

Unfortunately, Nochu is not US but Japanese, and it is not 2023 but rather 2024, when the high-rate disaster of 2023 was supposed to be over. Supposed to be... but instead it's only getting worse. Regular readers will hardly need it, but for novices Nikkei gives the following quick primer: "Interest rates in the U.S. and Europe have risen and bond prices are down. This reduced the value of high-priced (low-yielding) foreign bonds that Norinchukin purchased in the past, causing its paper losses to swell."

So faced with no other options, Nochu is doing the only thing it can: an orderly liquidation of tens of billions of securities now, when they are still liquid and carry a high price, in hopes of avoiding a disorderly liquidation and much worse, in a few months when the bond market freezes up.

And yes, the Japanese rates canary is quite, quite massive: as of the end of March, Norinchukin had approximately 23 trillion yen of foreign bonds (about $150 billion), amounting to 42% of its total 56 trillion yen of assets under management.

To get some sense of the scale, according to the Bank of Japan, outstanding foreign bonds held by depositary financial institutions amounted to 117 trillion yen as of the end of March. Norinchukin, which is a major institutional investor in Japan, holds as much as 20% of the total on its own! And those asking, yes: once Nochu begins selling, all others will have to join the club!

But why start the selling now? Because, as we warned last October when we predicted that the next bank crisis will be in Japan, the Japanese mega-bank now believes interest rate cuts in the U.S. and Europe are likely to take longer than it previously expected, it will try to significantly cut its unrealized losses by selling foreign bonds in fiscal 2024.

And so, Norinchukin plans to sell over 10 trillion yen in foreign bonds, in addition to its normal trading activities.

The rest of the story is filler: in attempt to divert attention from the 10 trillion yen elephant in the room, the Nikkei then wastes time discussing the bank's other "alternatives" to wit:

The company is now considering investment alternatives, including equities, corporate bonds, corporate loans and private equity, as well as securitized products such as corporate loan-backed securities and mortgage-backed securities. By diversifying its portfolio, it aims to prevent unrealized losses from expanding to the point where they become a concern for management. It will also try to replace some low-yielding foreign government debt with other such bonds offering higher interest rates.

What are you talking about? What diversification? Once the selling begins, the bank will be lucky if it can get even a fraction of the proceeds it hopes for (because all the other banks won't just be standing there twiddling their thumbs, as they wait to see how massively Nochu reprices the market).

And it's not just banks: if and when the selling begins by a bank that holds 20% of all foreign bonds in Japan, the liquidation cascade will quickly spread to Mrs Watanabe. According to the U.S. Treasury Department, Japanese investors held $1.18 trillion of U.S. government bonds as of March, the largest slice among foreign holders.

Needless to say, but the Nikkei does so anyway, "Massive sales by Norinchukin could have a sizable effect on the U.S. bond market."

And since we now know what is happening, it is only a matter of time before everyone else frontruns Norinchukin.

What happens next will be even uglier: since the bank will no longer be able to mask its fixed income losses under the guise of accounting sleight of hand, the bank's financial results for the period ending March 2025 will "deteriorate significantly as a result of the huge divestment of foreign bonds and turn paper losses into real ones." As of May, Norinchukin put its final loss at more than 500 billion yen, but this is now expected to reach the 1.5 trillion yen level.

A little more context: back in the immediate aftermath of the global financial crisis, in the year ending March 2009, Norinchukin posted a final loss of about 570 billion yen due to impairment of securitized products. The forecast loss for this fiscal year is expected to top the previous record by roughly 1 trillion yen. Nevertheless, Oku said that putting the losses on the books in the year ending next March will "improve [the bank's] finances and portfolio, thus enabling to move into the black in the period ending March 2026."

Spoiler alert: no it won't... and that's why the bank is now scrambling to share the pain with even greater fools, i.e., "investors."

According to the Nikkei, Norinchukin Bank is considering raising 1.2 trillion yen to shore up its finances. It has already started discussions with Japan Agriculture Cooperatives, one of its main investors, and others. Of course, the question of who in their right mind would lend the bank good money to plug an even bigger hole that is about to open up, is anyone's guess.

But that won't stop the bank from doing what it has to, now that it has picked the liquidation route: and once the selling flood begins, it won't end as these flashing red headlines from Bloomberg just confirmed:

- *NORINCHUKIN TO SELL US, EUROPEAN SOVEREIGN BONDS GRADUALLY

- *NORINCHUKIN ALSO WEIGHS LOCAL, OVERSEAS BONDS, PROJECT FINANCE

- *NORINCHUKIN EYES ASSETS INCLUDING CLOS, STOCKS AFTER BOND LOSS

There's a name for this: a firesale, but - drumroll - a "gradual" one, because that's how firesales supposedly go in Japan.

Luckily, the one thing nobody has to guess, is what happens next: as the wonderful movie Margin Call laid out so very well, once you realize that the music has stopped, you have three choices: i) be first, ii) be smarter, or iii) cheat. In the case of Japan's Norinchukin, it has decided the time has come to liquidate before everyone else. We wonder how "everyone else" will take this particular news...

No comments:

Post a Comment